Kapitalmarktausblick 11/2024

Nach dem Wahlsieg von Donald Trump: kommt jetzt der große Boom in den USA?

29.11.2024

In wenigen Wochen tritt der designierte künftige US-Präsident Donald Trump sein Amt an. Dieser ist ein erfolgreicher Unternehmer, der genau das Richtige tun wird, um die US-Wirtschaft stark wachsen zu lassen. Dann kann ja nichts mehr schiefgehen, oder?

Executive Summary:

Zwischen der aktuellen Situation am US-Kapitalmarkt, nämlich einer seit Jahren im internationalen Vergleich besonders starke Aktienkursentwicklung, Immobilienpreis- und Wechselkurssteigerung bei gleichzeitig sehr hoher Bewertung dieser Anlageformen, und der Lage in Japan vor 1990 bestehen auffallende Parallelen, bis hin zum Narrativ, das diese Ausnahmeerscheinungen erklären soll. Inwieweit auch die weitere Entwicklung in Japan ab 1990, nämlich eine besonders schwache Entwicklung von Aktienkursen und Immobilienpreisen, sich in den USA wiederholen könnte, hängt auch davon ab, ob die Wirtschaftspolitik von Trump die Konjunktur und die Kapitalmärkte fördert. Dies ist jedoch eher unwahrscheinlich. Hohe Zölle gingen in den letzten 175Jahren in den USA mit geringen Aktienerträgen einher. Außerdem wirken sie tendenziell inflationär und könnten damit eine ungünstige Zinsentwicklung auslösen. Auch die Verringerung der Zahl von Arbeitskräften durch die geplante Massenabschiebung von Einwanderern ist für die US-Wirtschaft eindeutig schädlich. Unternehmenssteuersenkungen können die Staatsschulden der USA weiter in gefährliche Höhen treiben. Schließlich ist auch Deregulierung nicht eindeutig positiv, wenn sie von Politikern wie Donald Trump und dem Neu-Politiker Elon Musk durchgeführt wird, die vor allem eigene Interessen verfolgen.

In wenigen Wochen tritt der designierte künftige US-Präsident Donald Trump sein Amt an. Dieser ist ein erfolgreicher Unternehmer, der genau das Richtige tun wird, um die US-Wirtschaft stark wachsen zu lassen. Dann kann ja nichts mehr schiefgehen, oder?

Dies dürfte tatsächlich das aktuelle Narrativ am amerikanischen Aktienmarkt sein. Die US-Aktienkurse sind auch im Novemberdeutlich angestiegen, während der Rest der Welt eher verhalten auf den Wahlsieg Trumps reagiert hat (Grafik 1). Der Haupttreiber waren dabei Informationstechnologie (IT)-Aktien, die bekanntlich in den USA besonders starkvertreten sind und den dortigen Aktienmarkt beflügelt haben, auch aufgrund der aktuellen Euphorie rund um das Thema Künstliche Intelligenz. Die Aktienkursgewinne sind in den USA seit 2019 auch wesentlich höher als die Anstiege der Fundamentaldaten der Unternehmen (Dividenden, Bruttogewinne bzw. Cash Earnings und Buchwerte, Grafik 2), so dass IT- und US-Aktien sehr teuer geworden sind, während Aktien im Rest der Welt ungefähr im Einklang mit den Fundamentaldaten gestiegen sind. Man erwartet demzufolge nur für die US-Wirtschaft Goldene Jahre, während im Rest der Welt Stagnation angesagt ist.

Bei den Wohnimmobilienpreisen lassen die USA den Rest der Welt ebenfalls hinter sich (Grafik 3); die Preise sind weitaus schnellergestiegen als die Fundamentaldaten, die bei Immobilien aus den Mieteinnahmenbestehen (Grafik 4).

Nur Japan kann bei der steigenden Bewertung von Immobilien mit den USA mithalten; Japan kommt jedoch nach dem Crash der dortigen Immobilienblase am Anfang der 90er Jahre von einem sehr tiefen Preisniveau, sodass hier ein überproportionaler Anstieg der Immobilienpreise im Vergleich zu den Mieteinnahmen verständlich ist (Grafik 5).

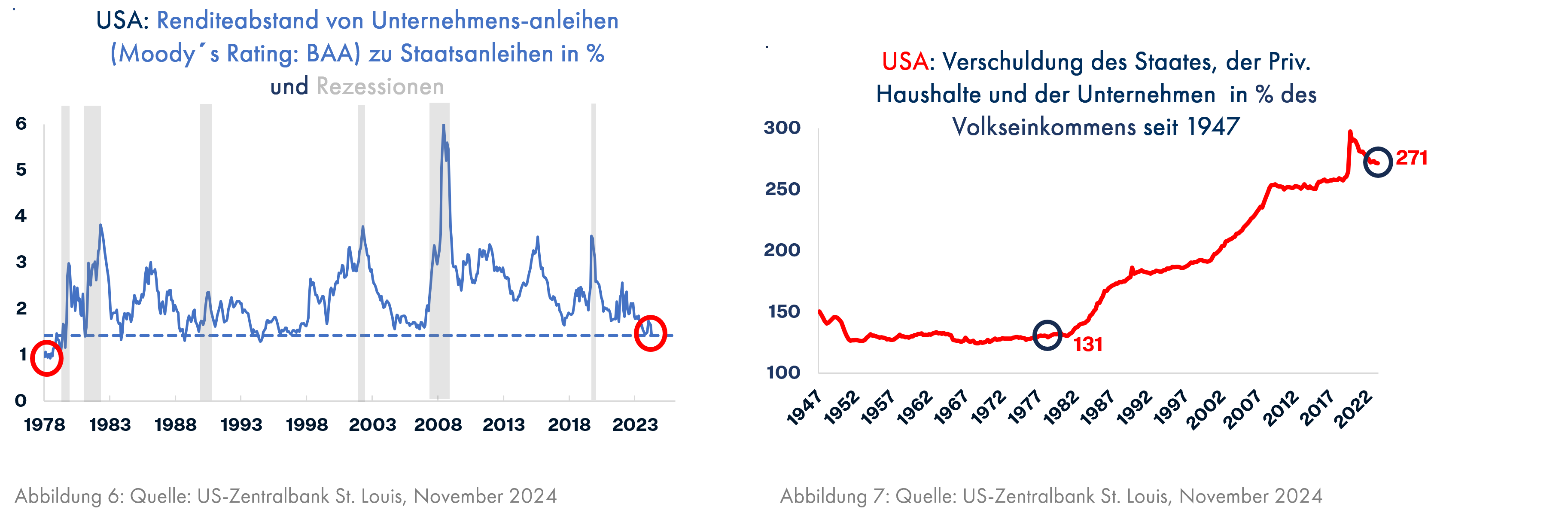

Eine gewisse Sorglosigkeit zeigt sich in den USA auch bei der Rendite von Unternehmensanleihen guter Bonität. Grafik 6 zeigt den Renditeabstand von Unternehmensanleihen mit einem Rating von BAA der Ratingagentur Moody´s. Dieser war in den letzten 45 Jahren nur vor 1998 für einige ganz kurze Zeiträume auf einem ähnlich niedrigen Niveau wie im November2024 nach der US-Wahl. Bis in die späten 70er Jahre gab es häufiger niedrigere Renditeabstände als heute, aber damals war auch die Gesamtverschuldung der USA(Unternehmen, Private Haushalte, Staat) weniger als halb so hoch wie heute(Grafik7). Dementsprechend waren auch die Risiken für die wirtschaftliche Stabilität geringer. Falls die US-Wirtschaft entgegen den allgemeinen Erwartungen demnächst eine Rezession erlebt, würden die Renditeabstände deutlich ansteigen und Unternehmensanleihen kräftige Kursverluste hinnehmen müssen.

Auch der Wechselkurs der US-Währung spiegelt eine optimistische Einschätzung der künftigen Entwicklung der USA im Vergleich zur Eurozone wider (Grafik 8). Die statistische Analyse zeigt aber, dass auf eine hohe Bewertung des US-Dollars gegenüber dem Euro anhand der Kaufkraft (relative Entwicklung der Inflationsraten in den USA und in der Eurozone) in den folgenden 10 Jahren Wechselkursgewinne des Euros zum US-Dollar folgen werden. Die aktuelle Überbewertung deutet auf Kursgewinne des Euros um knapp 4% p.a. bis2034 hin (Grafik 9).

Gegenüber dem japanischen Yen ist der Dollar noch stärker überbewertet (Grafik 10). Einer der Gründe dafür ist die seit der Finanzkrise2008 rasant wachsende Netto-Auslandsverschuldung der USA (Grafik 11). Wenn das Ausland Geld an einen US-Schuldner (Staat oder Unternehmen) verleiht, muss der Kreditgeber zunächst seine Euros oder Yen in US-Dollar tauschen, bevor er sie in den USA verleihen kann. Damit entsteht eine Dollarnachfrage, solange die Auslandsverschuldung der USA zunimmt. Bei einem aktuellen Niveau von 79% des US-Volkseinkommens handelt es sich um über 20.000 Mrd. US-Dollar, die inzwischen auch hohe Zinskosten verursachen. Sollten die Gläubiger der USA irgendwann einmal Geld zurückverlangen, wird der Dollar deutlich fallen müssen. Die hohe Bewertung der US-Währung ist also nicht unbedingt ein Zeichenstrotzender Gesundheit. Dementsprechend ist in Ländern, die ihr Netto-Auslandsvermögen erheblich gesteigert (Deutschland und Japan) bzw. ihre Auslandsverschuldung vollständig abgebaut haben (Italien), die Währung seit Jahren schwach.

Nun werfen wir einen Blick in die Vergangenheit, als schon einmal ein Land die führende weltweite Technologieführerschaft inne hatte, nämlich Japan. Dies belegt ein Zitat aus der Zeitschrift „Computerwoche“ vom13. Dezember 1991: „In den 90er Jahren wird sich entscheiden, welche der beiden Nationen künftig den Ton in der Computerindustrie angibt. Dabei stehen die Chancen für die Japaner gut, auch hier den Amerikanern den Rang abzulaufen“. Dieser weltweite Optimismus über Japans technologische Fähigkeiten liefert die Erklärung dafür, warum Japans Aktienmarkt in den 80er Jahren dem Rest der Weltdavongeeilt war. Wenn man Grafik 12 bis zum schwarzen Balken (Dezember 1989)mit Grafik 1 vergleicht, sieht man, dass die heutige IT-Branche und auch der US-Aktienmarkt wie damals Japan eine enorme Outperformance erreicht hat. Allerdings war diese in Japan nicht nachhaltig (Grafik 12, rechte Hälfte), weil die Kurse anders als in den übrigen Ländern wesentlich stärker gestiegen waren als die Fundamentaldaten; japanische Aktien waren im Dezember 1989 weitaus teurer als der Rest der Welt geworden (Grafik 13 bis zum schwarzen Balken),genau wie heute IT- und US-Aktien (Grafik 2). Nach 1989 entwickelten sich sowohl die Aktienkurse als auch die Bewertung in Japan wesentlich schwächer als im Rest der Welt.

Die hohe Bewertung in Japan war nicht nur durch die Technologiefantasie der Investoren entstanden, sondern auch durch hohe kreditfinanzierte Börsenspekulationen von japanischen Firmen am Aktienmarkt, weil man Aktien zum Tages- oder zum Kaufkurs bilanzieren durfte und dabei den höheren Kurs wählen konnte. Damit erschienen Aktienspekulationen risikolos, aber am Kursgipfel war die Dividendenrendite mit 0,4% nur noch ein Bruchteil der Kreditzinsen, die ungefähr das Zwanzigfache betrugen, und die Aktienkäufe wurden beendet, weil sie nun hohe Verluste aufgrund der Zinskosten verursachten. Sollten sich die hohen Investitionen der heutigen Technologiegiganten in die Entwicklung der künstlichen Intelligenz als renditeschwach herausstellen, dürften hohe Abschreibungen auf die Gewinne drücken. Auch Trumps künftige Zölle werden einige Technologiefirmen wie Apple, Tesla und Nvidia belasten, da diese Firmenerhebliche Importe aus China benötigen, die sich dann verteuern werden.

Eine weitere Parallele besteht darin, dass sich auch der japanische Immobilienmarkt infolge der allgemeinen Euphorie stärker entwickelte als die Immobilienpreise im Rest der Welt (Grafik 14, siehe entsprechend dazu Grafik 3). Ebenso stieg die Bewertung von japanischen Wohnimmobilien im Vergleich zu den Mieteinnahmen bis zum Dezember 1989 – wie heute in den USA –stärker als in den anderen Industrieländern (Grafiken 15 und 4).

Schließlich wertete der japanische Yen gegenüber dem Dollar und dem (zurück gerechneten) Euro in den 80er Jahren deutlich auf (Grafik 16).Aktuell hat der Dollar in den letzten Jahren gegenüber dem Yen und dem Euroaufgewertet (Grafiken 8 und 10).

Damit weist die Lage Japans in den 80er Jahren erhebliche Parallelen zu der aktuellen Situation in den USA auf.

Bis hierher lautet das Zwischenfazit, dass in den USA Aktien, Wohnimmobilien, Unternehmensanleihen und die Währung überbewertet und die künftigen Ertragserwartungen unterdurchschnittlich sein dürften. Könnte sich dieses Szenario durch die Wahl von Trump verändern?

Dazu betrachten wir nachfolgend die möglichen Auswirkungen der von Trump versprochenen Maßnahmen.

Die geplante Abschiebung von Millionen Einwanderern hat mit Sicherheit negative Folgen für die US-Wirtschaft. Immigranten in den USA wandern nicht wegen üppiger Sozialleistungen ein, sondern weil sie für sich und ihre Familien durch harte Arbeit eine Existenz aufbauen wollen.

Die Deutsche Bank hat in seiner Studie die - nicht überraschenden – Folgen berechnet. Demnach führt ein Rückgang der Zahl der Menschen im arbeitsfähigen Alter zu einem Rückgang des Wirtschaftswachstums(Grafik 17). Auch wenn man das Wirtschaftswachstum pro Kopf heranzieht, ändert sich an dieser Tendenz nichts (Grafik 18). Ein Rückgang der Anzahl der Menschen im arbeitsfähigen Alter relativ zu den über 65-jährigen, der bei einer Ausweisung der zumeist jüngeren Einwanderer entstehen würde, würde ebenfalls das Wirtschaftswachstum beeinträchtigen (Grafik 19).

Millionen von Arbeitskräften auszuweisen ist exakt das, was die USA zur Zeit nicht brauchen.

Dies gilt auch für die Erhebung hoher Zölle. Zölle wirken zunächst inflationstreibend, weil der gewünschte Effekt ja genau darin besteht, dass ausländische Waren teurer und damit unattraktiver für die amerikanischen Käufer werden. Bei höherer Inflation besteht aber die Gefahr, dass die Zinsen in den USA steigen könnten, was in der Eurozone angesichts der schwachen Wirtschaft nicht passieren wird. Eine steigende Zinsdifferenz dürfte den Dollar zumindest kurzfristig weiter nach oben drücken (Grafik 20), aber steigende Zinsen würden die US-Wirtschaft belasten.

Grafik 21 zeigt die Zolleinnahmen der US-Regierung seit 1850in % des Importvolumens. Trumps Pläne würden die USA in die 30er Jahre zurückwerfen, als man während der Weltwirtschaftskrise ebenfalls glaubte, durch Zölle die US-Industrie schützen zu können. Daraufhin fielen die Importe und die Exporte der USA ebenso wie der gesamte Welthandel innerhalb von nur 3 Jahren um über 60%, was diese Krise zur schlimmsten Depression der US-Geschichte werden ließ. Der Anteil der Zölle an der Verschärfung der Krise wird als sehr hocheingeschätzt (Quelle: Wikipedia, Stichwort: Smoot-Hawley Tariff Act). Im 19.Jahrhundert waren Zölle ein wichtiger Bestandteil der Finanzierung des Staates, der nur sehr geringe Steuern erhob und glaubte, die junge heimische Industriedurch Zölle von der europäischen Konkurrenz abzuschirmen. Außerdem waren sie ein Instrument der Korruption. Präsidentschaftskandidaten boten Industrieunternehmen gegen Wahlkampfspenden Zollerhebungen an, die direkt gegen deren Konkurrenz gerichtet waren.

Auch der Aktienmarkt wird nicht von Zöllen profitieren. Nur in Zeiten niedriger Zölle (weniger als 10% des Importvolumens) liefert der Aktienmarkt hohe reale Kursgewinne in Höhe von fast 8% p.a. ab; schon bei den von Trump geplanten Zöllen sackt der jährliche Aktienkursgewinn um mehr als die Hälfte auf 3,6% p.a. ab (Grafik 22).

Die negativen Auswirkungen von Massenabschiebungen und hohen Zöllen ist so eindeutig, dass man dahinter in erheblichem Maße Wahlkampfparolen vermuten darf. Während der ersten Präsidentschaft von Donald Trump wurde wesentlich weniger verwirklicht als angekündigt worden war, z.B. beim Bau einer Mauer an der Grenze zu Mexiko.

Die von Trump geplante und am US-Aktienmarkt bejubelte massive Deregulierung wird nach einer Aussage des frischgebackenen Wirtschaftsnobelpreisträgers Daron Acemoglu (Wirtschaftsprofessor an der renommierten US-Universität MIT) nicht nur positiv sein, sondern zu einer Ausweitung betrügerischer oder einfach schlechter Produktangebote und Dienstleistungen führen, ebenso wie die Deregulierung des für Betrügereien bekannten Krypto-Sektors, der Donald Trump durch massive Wahlkampfspenden auf seine Seite gezogen hat (Quelle: Finanz und Wirtschaft, November 2024).

Die Senkung der Unternehmenssteuern von 21% auf 15% (Trump hat auch mal 20% genannt, weil es eine schöne runde Zahl ist) wird ebenfalls als Pluspunkt für den Aktienmarkt bewertet, ist allerdings aufgrund der ohnehin schon jetzt gefährlich hohen Staatsverschuldung nicht nachhaltig (Grafik 23).

Kurzfristig könnte Trump mit einer weiteren Erhöhung der Staatsausgaben, mit neuen Zöllen, die die Arbeitsplätze sichern und die Staatseinnahmen verbessern, und mit Steuersenkungen eine Stimmungsverbesserung bewirken. Diese hätte dann aber zur Folge, dass weitere Zinssenkungen nur noch in geringem Umfang oder gar nicht mehr erfolgen, was die Wirtschaft belasten würde. Die Hoffnung besteht darin, dass Trump seine Vorschläge nur in homöopathischen Dosen umsetzt und damit den Schaden gering hält. Die im Novemberveröffentlichten Frühindikatoren (Leading Economic Indicators, LEI) der US-Wirtschaft sind nämlich erneut gefallen (Grafik 24), ebenso wie in den beiden anderen großen Wirtschaftsräumen (China und Eurozone, Grafiken 25 und26), die unter den geplanten Zöllen besonders leiden würden. In keiner der dreigroßen Wirtschaftsregionen der Welt gab es in den letzten Jahrzehnten einen derart starken Rückgang der LEIs, ohne dass daraufhin eine Rezession eingetreten wäre.

Ebenfalls völlig außergewöhnlich ist der Anstieg der trendbereinigten Aktienkurse, während gleichzeitig die ebenfalls trendbereinigten LEIs fallen (rotes Feld am rechten Rand der drei Grafiken 27bis 29). Auch zuvor gab es in jeder Region eine (rosa) Phase mit gegenläufigen LEIs und Aktienkursen, aber da stiegen die LEIs und die Aktienkurse fielen. Allerdings scheint sich in der Eurozone der Einfluss der schwachen LEIs bereits bemerkbar zu machen, denn dort ist der Höhepunkt der Aktienkurse möglicherweise überschritten.

Fazit:

Die US-Kapitalmärkte (Aktien, Immobilien und Wechselkurse)weisen seit mehreren Jahren erhebliche Parallelen zu der ehemaligen Technologiehochburg Japan in den Jahren vor dem Dezember 1989 auf, insbesondere eine auffallend bessere Aktienkursentwicklung, aber auch eine wesentlich höhere Bewertung von Aktien, die dann ab 1990 in Japan zu einer sehr schwachen Aktienperformance beigetragen hat. Ebenso vergleichbar war die im internationalen Vergleich deutlich stärkere Immobilienpreisentwicklung und auch die Aufwertung der Währung. Auch das Narrativ, nämlich die Überzeugung, dass Hochtechnologie damals nur noch aus Japan kommen wird, ist mit der aktuellen unbestreitbaren Vormachtstellung der USA in diesem Bereich vergleichbar.

Nun hoffen viele Aktienkäufer darauf, dass Donald Trump eine unternehmensfreundliche Wirtschaftspolitik betreiben wird und sich damit der Höhenflug der US-Aktien fortsetzen kann. Leider sind die von ihm geplanten Maßnahmen entweder nicht dauerhaft durchzuhalten – hier ist die weitere Senkung der Unternehmenssteuern zu nennen, die sich die stark verschuldete US-Regierung nicht mehr leisten kann – oder sie sind für die US-Wirtschaft sogar schädlich. An erster Stelle ist hier die angedrohte Massenabschiebung von Einwanderern, die zumeist auch Arbeitskräfte sind, zu nennen. Arbeitskräfteknappheit und höhere Inflation wegen stärkerer Lohnsteigerungen wären die zu erwartende Folge. Ebenfalls klar inflationär und auch negativ auf die Aktienkursgewinne wirken Zölle, die ausländische Waren in den USA teurer machen und dadurch die Kaufkraft der amerikanischen Konsumenten schwächen und durch Gegenzölle auch die US-Firmen schädigen. Mehr Inflation bedeutet weniger Zinssenkung oder sogar höhere Zinsen; beides wäre schlecht für die US-Konjunktur, deren Frühindikatoren ohnehin auf rezessive Tendenzen hindeuten. Deregulierung wäre eigentlich eindeutig positiv, da Bürokratie auch in den USA ein Problem ist, aber nur, wenn sie von seriösen Politikern durchgeführt wird, die vor allem das Allgemeinwohl im Auge haben. Diese Voraussetzung erfüllen Donald Trump und Elon Musk, der Deregulierungsbeauftragte, nicht in ausreichendem Maße.

Konsequenzen für das Portfolio

- Aktien: Die derzeitige Überbewertung von US-Aktien, insbesondere im IT-Sektor, erfordert Vorsicht. Investoren sollten ihre Positionen diversifizieren und auf Regionen und Sektoren setzen, die weniger überhitzt sind, etwa Europa oder Schwellenländer. Kurzfristig könnten defensive Branchen wie Gesundheitswesen oder Basiskonsumgüter Sicherheit bieten. Wir sind in Aktien untergewichtet und halten dafür mehr Liquidität. Innerhalb der Aktien haben wir die USA zugunsten aller anderen Regionen untergewichtet und halten etwas mehr defensive Sektoren.

- Unternehmensanleihen: Die aktuell niedrigen Renditeabstände bei Unternehmensanleihen deuten auf ein erhöhtes Risiko hin. Für den Fall, dass die US-Konjunktur in eine Rezession rutscht, sind deutliche Kursverluste zu erwarten. Dies könnte dann ein guter Zeitpunkt für einen Wiedereinstieg sein. Aktuell meiden wir Unternehmensanleihen.

- Gold: Gold bleibt eine wichtige Absicherung gegen Inflation, politische Unsicherheit und Währungsrisiken. Investoren sollten eine strategische Position in Gold halten, idealerweise 5–12% des Portfolios.

- Immobilien: Die US-Wohnimmobilienmärkte sind stark bewertet, und eine Korrektur ist nicht auszuschließen. Globale Diversifikation in stabileren Immobilienmärkten kann das Risiko reduzieren.

Abschließend unsere Kernaussagen aus dem Kapitalmarktausblick vom November 2021, den Sie hier finden:

Vor 3 Jahren untersuchten wir erstmals die Lage in China und kamen zu dem Schluss, dass China vor enormen Problemen steht, weil am Immobilienmarkt sehr viel Kapital für leerstehende Wohnungen verschwendet wurde. Auch die schwierigen Lebensbedingungen, z.B. immer noch völlig überteuerte Wohnimmobilienpreise und hohe Kosten für die Bildung und infolgedessen stark sinkende Geburtenzahlen wurden dargelegt. Im Ergebnissagten wir voraus, dass auch China künftig die Wirtschaft verstärkt durchstaatliche Hilfen wird stützen müssen und der historisch beispiellose Boom zu Ende geht.

Den Kapitalmarktausblick können Sie auch hier herunterladen.